Today on Product Saturday: Databricks introduces an open-source proposal for sharing corporate data, Datadog adds more bits to Bits AI, and the quote of the week.

Today: Anthropic's first Mythos-class AI model launch did not sit well with a lot of enterprise users, Oracle investors remain wary about its expansion plans, and the latest enterprise moves.

Today: Microsoft scrambles to minimize the fallout from a second batch of compromised open-source patches in a month, Apple teams up with Google for an expansion of its cloud security service, and the latest funding rounds in enterprise tech.

Tomasz Tunguz: Enterprise tech is "going to be a lot choppier"

Deep down, most people knew it couldn't last. But the remarkable run enjoyed by enterprise software companies and their investors over more than a decade came to an abrupt end in 2022, and the new order is still sorting itself out.

Deep down, most people knew it couldn't last. But the remarkable run enjoyed by enterprise software companies and their investors over more than a decade came to an abrupt end in 2022, and the new order is still sorting itself out.

Tomasz Tunguz invested in many winners from that era over 14 years at Redpoint Ventures, including Looker, Stackrox, and Kustomer, but decided to strike out on his own after realizing that enterprise software investing needed to change. Theory Ventures, introduced last month, is a reflection of his philosophy that the venture capital business needs to pare down and focus on supporting a small number of companies as they grow, rather than scattering what felt like unlimited money in the zero-interest rate era across hundreds of companies knowing most would fail and a few would hit the jackpot.

"Our goal is not to be in every great company but to make sure all the companies we invest in are great," Tunguz said in a recent interview. "By remaining small, having a really small portfolio and focusing on a set number of spaces, we don't have to cover everything."

Over the course of a wide-ranging discussion, Tunguz explained why SaaS companies are raising prices, why companies that can shorten notoriously long enterprise sales cycles are thriving, and the three technology areas he's focused on as Theory Ventures starts to deploy capital.

This interview has been lightly edited and condensed for clarity.

What changed over the last year, and how did it change your approach to investing?

So, since 2010, let's call it, we've had the longest bull market in US history, and the cost of capital has gone way down. And so the venture capital ecosystem in the US has grown from about $8 (billion) to about $320 billion, and then we'll fall to about $180 to $200 (billion) this year.

When you have a bull market like that, people will stop paying attention to fundamentals. And that was true, as much with startups as it is with venture firms, because venture firms also have business models.

Tomasz Tunguz, general partner, Theory Ventures

The idea with Theory was to create a venture firm that would thrive within that capital markets environment. We don't invest in many companies. A lot of venture portfolios will have 30 to 50 companies; we'll have 12 to 15. And the thesis-driven approach allows us just to understand the space deeper, and then also have more capital to support those companies as they grow through all the ups and downs.

We're not going to have an unmitigated bull market for 10 years over the next decade, it's going to be a lot choppier. So you I think, one of the value propositions for VCs that hasn't been important historically, or in the last 10 years, is the amount of reserves and follow-on capital that they can command for their portfolio.

Would it be right to say that it's like more wood behind fewer arrows?

That's the whole idea.

That puts more emphasis on making sure that those arrows land in the place you want them to land. Right now it's been a lot of, "just invest in everything, and you know that nine of those might fail, but the 10th one will go huge." That's the whole business model, but you're doing something different. So how do you make those calls?

The reason the firm is called Theory is because we do a lot of work, we do a lot of research in building our thesis. Our goal is not to be in every great company but to make sure all the companies we invest in are great. By remaining small, having a really small portfolio and focusing on a set number of spaces, we don't have to cover everything.

So if we can go deep within a space, identify all the key companies and figure out what the buyers want — it's all B2B — understand what are the main specifications or criteria that buyers are using to evaluate, and then find the best company and then be able to support them through multiple stages. The startup benefits, because they've got a board member who understands their space at a really deep level, and then they have a capital partner who can continue to help them grow as they scale.

A lot of VCs I've talked to in the past often talk about how they bet on teams, or they bet on founders, more than they bet on products or technologies. Is that part of your thinking here?

I had a marketing professor in college, a Belgian guy, who put an equation on the board, which was innovation equals invention plus distribution. The idea is, the only way to change the world is you have to create something new and then you have to explain it to people in a way that they want to buy it. And the way that we think about the world is both of those components are essential.

But distribution actually matters a bit more than the technology. If you think about VHS/Betamax, that's played out time and time again. The thing that we're really looking for are these technology innovations that create go-to-market advantages.

What are some examples of that? You know, the technologies that you're looking at that you think have that go-to-market advantage?

One was Looker. So that was a big company that Google bought, and they were the first BI tool that was architected to operate on cloud data warehouses. Nobody else could manage the scale at the time. Because of that technology, they were able to go to market with Snowflake and BigQuery, and Redshift, and they grew really fast.

The question is, is this increasing revenue or is this decreasing costs? If you can't answer that question in a very concrete way, then you're in trouble.

There's another company that I work with called Spot AI that's in the video surveillance space. It's an ex-Meraki team, and they have a technology that they connect to all the different physical security cameras that a business might have. Because of their networking background, it's super easy, so the deployment takes less than five minutes. And because the deployment is so fast, they're able to sell that product really fast; when we led the seed, (they had) 14-day sales cycles, which is really unusual. Most of the time you see multiyear sales cycles in that category.

Is that something specifically you're looking for, a faster sales cycle? Enterprise buying patterns are glacial and from what I understand that's only gotten worse over the last year.

Faster sales cycles are really awesome for many reasons.

One is (that) faster feedback loops lead to faster iteration. If you just think about a learning cycle, if you can learn (something) every day, as opposed to learning it every three months or every six months, you're just going to be better. The second reason that fast sales cycles are really good is it helps account executives ramp up, so you can start to scale a sales team much better. And then the third reason is you get money. Your cash collections tend to be significantly better in shorter sales cycles. That's an important criterion, particularly in this environment where CFOs are clamping down on a lot of excess spending.

There are a lot of companies that started over the last five years selling into this enterprise market and are now confronted with this longer sales cycle trend, thanks to broader economic worries. What should they do to push through that?

When you're selling software, you're selling a promotion; the person who's buying the software is hoping to get promoted. And they do that one of two different ways: They make more money for the business, or they materially reduce the cost of the business.

In 2008, a lot of the startup pitches, when I joined the business, they were focused on "we increase revenue or we decrease cost." And in the last 12 years, we've seen this "thousand flowers bloom" (approach) in software where that ROI calculation didn't need to be justified. It just didn't, because everything was growing, and there was lots of money and the money was cheap.

So you could have three different chat applications and four different collaboration applications and two different customer support (tools): It doesn't matter. But now when the CFO and the office of the CFO says, "we need to get to profitability," now the software is being examined. And the question is, is this increasing revenue or is this decreasing costs?

If you can't answer that question in a very concrete way, then you're in trouble. The companies that are the most insulated today are the ones who say, "you're spending lots of money on your data infrastructure, you're spending lots of money on your security infrastructure, we can help you reduce that by 30%." Those sales cycles, they are really fast. The cost-reduction value proposition right now is the one that resonates the most with buyers, just given the macro.

At the same time, I'm hearing a lot of SaaS companies are actually significantly raising prices. It's a rude surprise for a lot of people who were on the buying side who were used to a certain level of spend and are now looking at significant increases.

I think a lot of companies are using inflation as a way of justifying it. The other justification internally is new customer acquisition is slowing down meaningfully, because the sales cycles are slower. Just to make this point really clear …

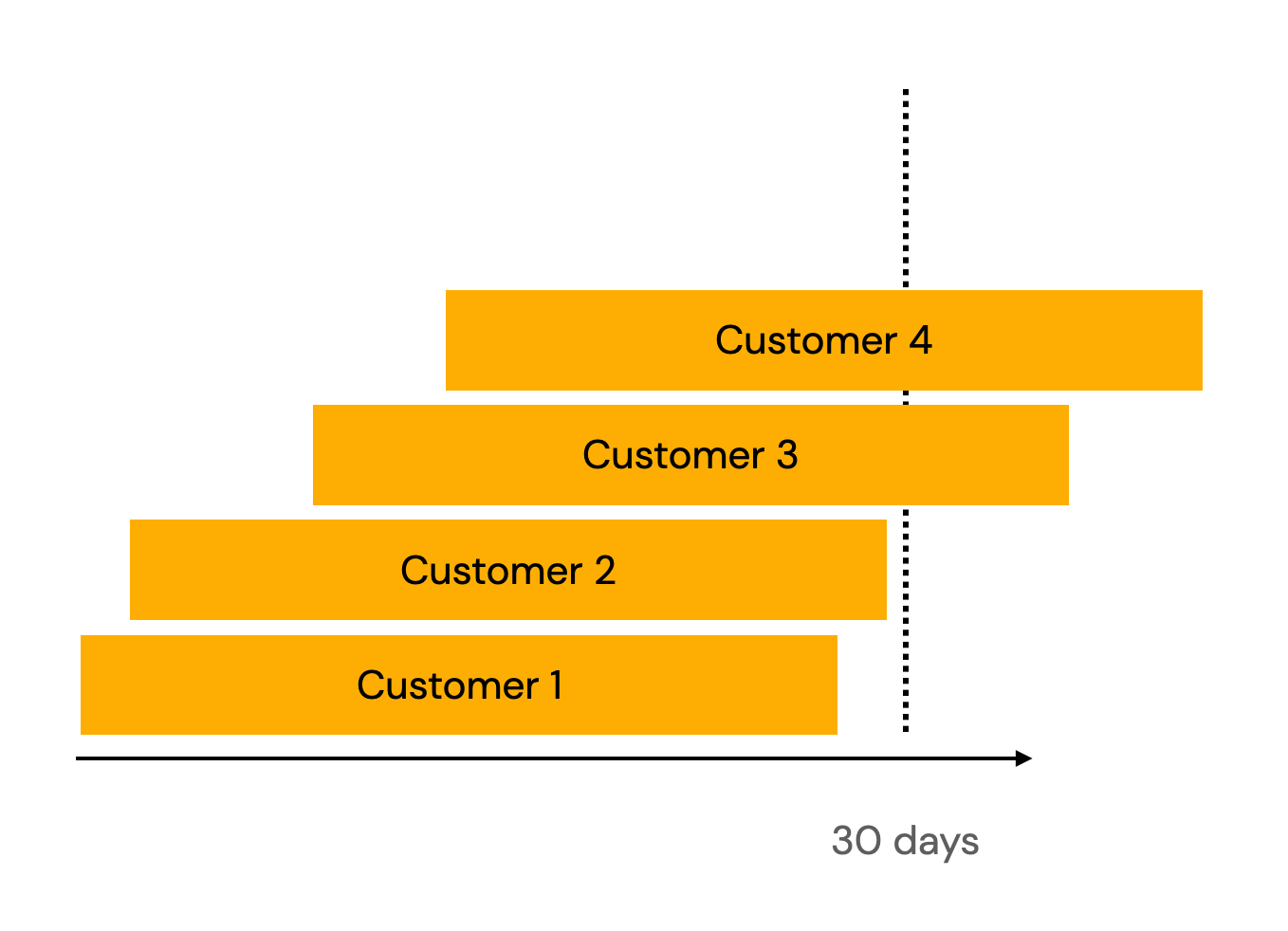

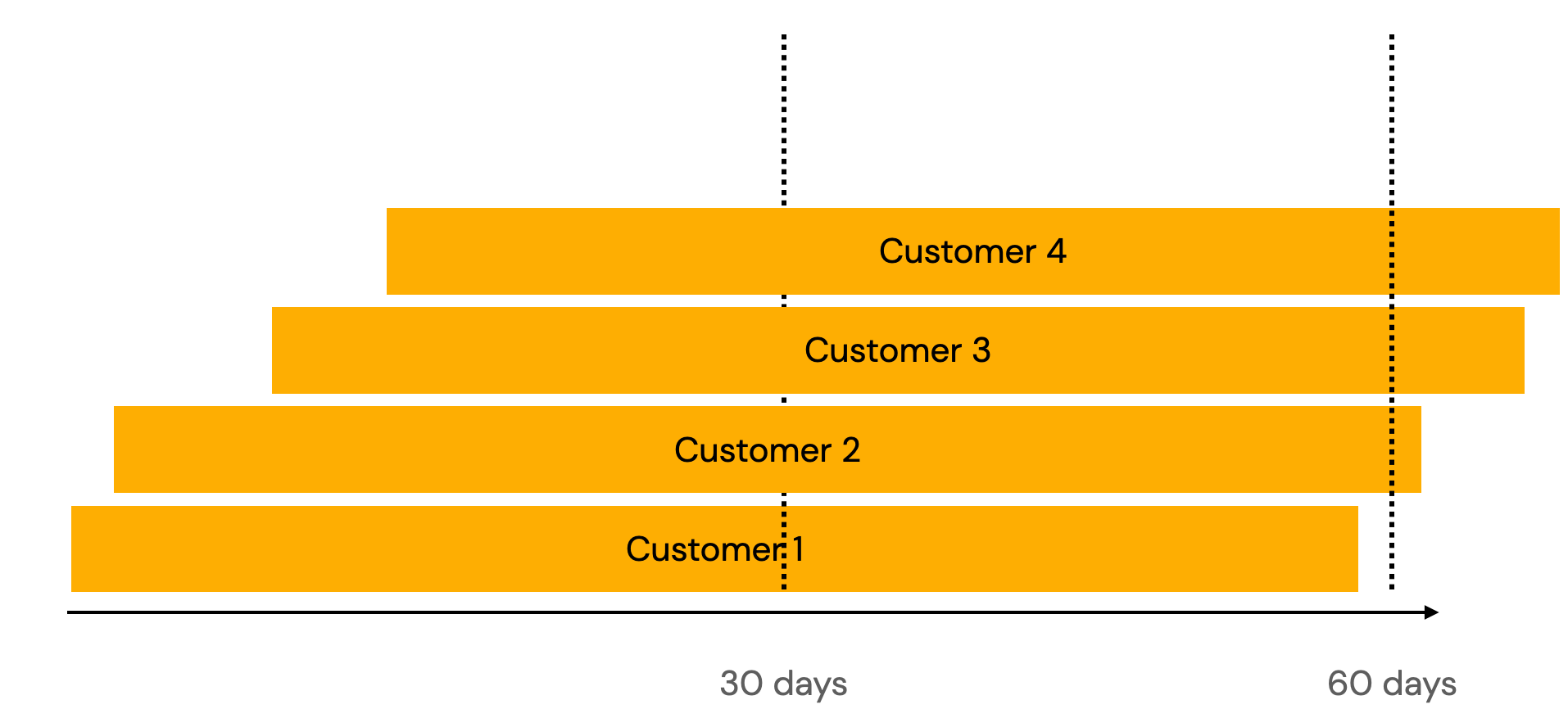

(shares screen)

Let's say you've got four customers in the pipeline, and your sales cycle is about 30 days. If your pipeline looks like this, you've closed customer one and customer two, and then three and four will slip into the next period. But if you double the sales cycle, then what happens is you booked zero in the first 30 days, you book only one deal in the next period. And so you've gone from booking two customers per period to zero customers and one customer per period.

If you're in that situation, and you need to grow, well, you've got to make more money from your existing users. So how will you do that? You'll raise prices.

A lot of software companies, they target 50% of their growth is coming from new customers, and about 50% is coming from existing customers. That's switching now, you're going to see more companies where the growth is driven by the existing customer base, as opposed to new logos.

From a technology standpoint, what are you looking at right now? If I hear the term generative AI one more time, I think I might lose my mind. But there's clearly a groundswell of interest in that as a technology and that as an investment space. What are you looking at that gets you excited? What do you think is maybe a little overhyped? And what's real?

So there are three categories.

One is just companies in and around data. Data volumes are growing at 45% a year, and so people are spending more and more time, effort, and dollars in order to understand and get value from it. We've got a theme called the decade of data, and that's not changing.

Machine learning is another one. The generative stuff is exciting; Goldman put out a report saying that that technology alone could increase US GDP between 1.5% to 2.9%, which would double US GDP growth, which is a really big deal. It's about 1,000 times more than the personal computer impacted GDP growth. This is why people are so excited about it.

I think the other impact of generative AI is that there are three other kinds of machine learning. There's classification, which is what Google uses for ads; there's prediction: "What's the weather?" and then there's natural language processing: "OK Siri." All of those technologies are going to benefit from the halo that Gen AI is casting.

And then the last category — and this is a category where two years ago it was the hottest thing — web3 technologies. The way I look at them is there were three big innovations that came out of web3; one is stablecoins, being able to move digital dollars around. And the other one is decentralized finance or defi, which is a new securities market. I'm not paying attention to either one of those — they're too highly regulated — but the last one is blockchains as databases.

If you plot the revenue of MongoDB and Ethereum, they correlate one to one. And if you visit Reddit, 95% of Reddit is running on AWS and then 5% is running on Polygon, but as a user, you wouldn't know. What that tells me is that these blockchains are databases for new kinds of applications. And the eternal question in that space has been "Well, what can you build there that you couldn't build in web2?" We're finally starting to get to that place.

Whether it's the next-generation advertising technology using decentralized infrastructure, it's like data sharing or healthcare, and I think there's a world — it's not an immediate future — but there'll be a world where Salesforce is re-architected in a way, or a CRM is built on decentralized infrastructure. And all of that is being catalyzed by more and more stringent regulatory regimes around data.

Can I go back to the database thing for a second? The pushback I would hear most often about blockchain in general is it's too slow to really compete with modern databases. Has something changed there?

Yeah, so there's two parts. One is the costs. So it used to be egas — Ethereum gas — was about $40 to $70 per transaction, now it's about $2. And then you have new layers on top that are called L2s where it's ninety-nine one-hundredths of a cent.

On the performance side, you have new blockchains, new databases that are optimized for speed. And so you can look like Aptos, or Mysten, and there are others. And so what you have now is you've got, just like in the web2 world, Glacier for really slow storage and then you have Redis for like super-optimal super-fast caching, and you've got a whole bunch of stuff in between. That's starting to happen in the blockchain space, where there are enough databases now for different kinds of applications.

I can't stand here and tell you, for every web2 database, there is a web3 equivalent. But we're getting there.

There are a lot of web2 databases. I think the question that I think a lot of us have been asking is like, OK, I can see the promise here with blockchain. But until it's a reasonable alternative to what I already have, I just don't really see a reason to change what I'm doing. And so you're saying that you're starting to see that?

Let's make this a little more concrete. So let's turn the clock ahead three years from now and you're Salesforce. The New York Times buys software from Adobe, and Adobe puts the New York Times information into Salesforce. That's now governed by a whole bunch of PII information. And so both Adobe and Salesforce are now on the hook for making sure that Adobe Germany, their data is stored in a German data center. And then Singapore has its own regulations, and California has specific regulations. So at some point, it just becomes impossible for a company not to take compliance risks, because of all these interlocking regulatory rules.

So what do they do instead? Well, they say, "New York Times, create an NFT." And within an NFT, there's the information of the people who bought the software, there are the wiring instructions, there's the addresses, there's all the key information that we need to know about that account; grant us access to it, and then our new Salesforce, our decentralized Salesforce, will read it. And if there is a point in time when the New York Times is no longer a customer, they just revoke access to the NFT. And because the New York Times has custody of their own data in that NFT, or whatever it will be, all of the regulatory challenges have gone away. And the New York Times is in control of its own data.

Everybody benefits from that kind of result. Now, how long will it take for us to get there? And will the architecture be like that? I don't know yet. But the broader trends are there: the databases are cheaper, the databases are faster, and the regulatory regimes are getting stricter and stricter.

The other big shift that's happening there is historically, web3 companies have sold to web3 companies. There are only about 53 web3 companies that generate more than 5 million on chain. So the market size is tiny. Now what's happening is as the tide of venture capital has left web3, a lot of these businesses now need to start generating revenue. And so they're turning their attention from web3 buyers to web2 buyers. That's a big change.

So those are our three big categories. One, I think there'll be software applications that are built on top of Snowflake and cloud data warehouses, so you're gonna see hybrid transactional systems. I think that the second one is the application of machine learning in novel ways. And then the third one is rebuilding software applications on a decentralized infrastructure.

Tom Krazit has covered the technology industry for over 20 years, focused on enterprise technology during the rise of cloud computing over the last ten years at Gigaom, Structure and Protocol.

Parikh, executive vice president of Microsoft's CoreAI group, leads a relatively new organization that is overhauling the way Microsoft develops software — both internally and for external customers — around the new capabilities that large-language models have brought to the command line.

Schmidt discussed the frequency and style of the attacks Amazon fends off every day, the capabilities that cybersecurity defenders can bring to bear thanks to generative AI, and the potential that machine-generated code could lead to the rise of a new class of software vulnerabilities.

Linear started off as an issue-tracking tool helping developers coordinate on eliminating blockers and fixing problems, but has expanded into a product-development system. "We have this fairly simple idea that engineering is really the front line of all this information," Saarinen said.

As worries about the economy accelerate, CIOs are regaining control over sprawling application footprints. According to McDermott, "What's happening is technology is the only way out. It's not kind of, sort of; it's the only way out."